How Tidspension works

Tidspension differs from other savings products. As a customer, you have two accounts: one for your contributions and one for your investment return.

Tidspension differs from other savings products. As a customer, you have two accounts: one for your contributions and one for your investment return.

You can shorten or extend the term of your Tidspension agreement, without any effect on your Pensionskonto (pension account) or Bufferkonto (buffer account).

Your Tidspension consists of two accounts: a pension account (P account) and a buffer account (B account). If you shorten or extend the term of your pension scheme, the amount in your P account and your B account, respectively, will not be affected. Your savings will be invested with due consideration to the new retirement age/and or payout schedule.

If you change pension provider and choose another savings product than Tidspension, or if you want to have your savings paid out, we will calculate your savings as the sum of the amounts in your P account and your B account.

This means that if the amount in your B account is negative on the date when you terminate the product, we will offset the balance of your B account against your P account. We will also do so if you have a Tidspension scheme with guarantee.

A Tidspension scheme with guarantee ensures that the annual return on your P account will never be negative.

Tidspension is a unit-linked product, in which the return is determined by investment market developments. With a guarantee, you protect yourself against the amount in your P account being reduced in years with negative investment returns.

With a Tidspension scheme with guarantee, you are guaranteed that you will not have a negative annual return on your P account during either the savings period or the payout period. Each year on 31 December, we make up the total annual return on your P account. We do this by adding up all monthly returns. If the amount is negative, the guarantee is activated, which means that a proportion of the negative amount is transferred back to the B account. Danica will pay the remainder. The closer you are to retirement, the larger the portion of the guarantee transfer will be paid by Danica.

The guarantee costs 0.5 percent of the annual amount in the P account.

During the payout period, you are also guaranteed an annual minimum payout from your annuity pension and life annuity. The guaranteed minimum payout is determined when you retire.

Despite the guarantee, the amount in your P account may be reduced during a calendar year due to expenses, payment for the guarantee, payouts and risk premium deductions.

The amount of pension benefits you receive when you retire depends on the balance of your pension account (P account). The amount in your buffer account (B account) is used to calculate future adjustments of your pension benefits.

Your benefits will be paid from your P account. Even though pension contributions are no longer made to your scheme, we will continue to invest your pension savings to generate a return for you. As was the case when you were saving up for your retirement, your total return will be placed in your B account. Every month, we ‘transfer’ the returns from the B account to the P account – just as we did when you were saving up for your retirement.

A special Tidspension equalisation mechanism ensures that your pension benefits are as stable as possible throughout the payout period.

Even though returns fluctuate from one year to the next, a stable return will be added to your P account from your B account. This means you will receive more stable benefits once you have retired. In a volatile market where benefits from a standard unit-linked product can fluctuate from year to year, Tidspension benefits will typically vary by only a few percent from one year to the next.

When you retire, we calculate your non-guaranteed benefits based on the following assumptions:

As the expected return on the P account is a factor in determining how much you receive, your benefits will be increased or reduced if the return on the P account is higher or lower than we had anticipated.

Changes in longevity will also have a positive or negative effect on your life annuity benefits if it differs from the longevity we have assumed.

If you have set up an annuity pension scheme and/or before 13 November 2009 made an agreement for life-long benefits, and if you have not subsequently attached a guarantee to your pension scheme, the assumptions may change once a year while you are receiving pension benefits.

If, on the other hand, you have attached a guarantee to your pension scheme, or if you have made an agreement for life-long benefits after 13 November 2009, the assumptions will remain fixed and cannot be changed while you are receiving pension benefits.

Your Tidspension consists of two accounts. One for your contributions and one for your annual return.

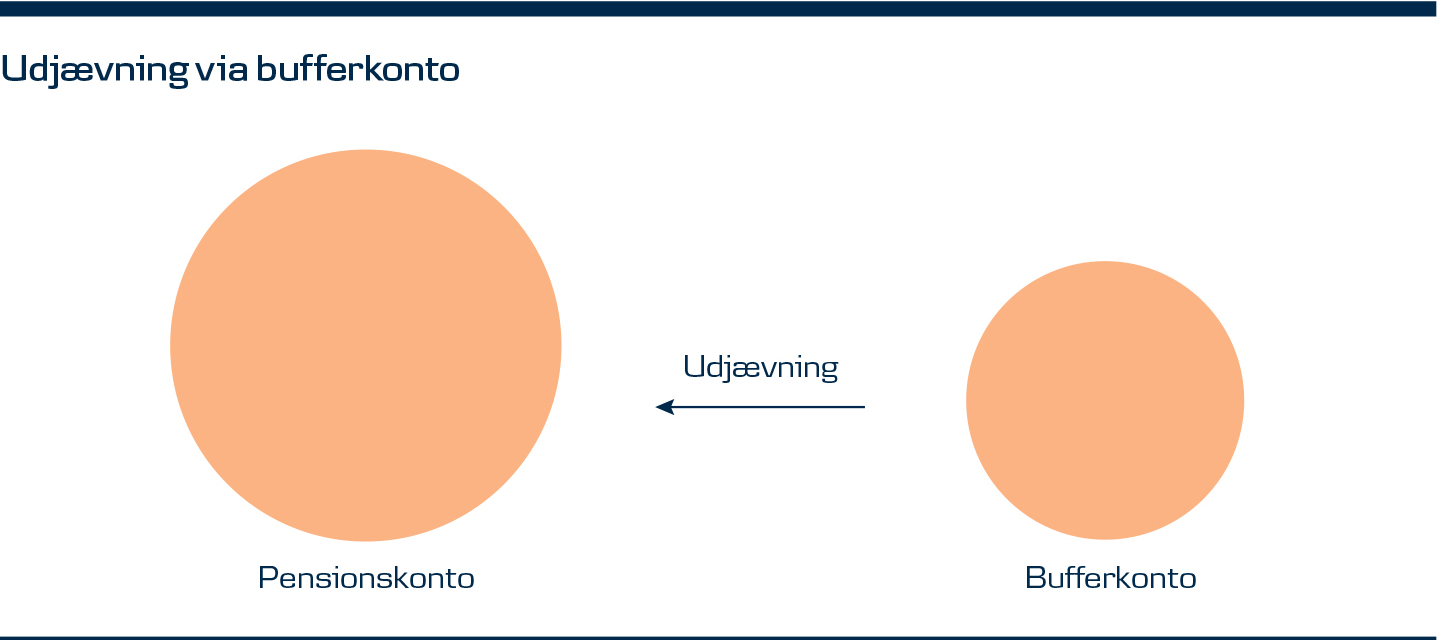

The pension account determines the amount of pension benefits. Even though investment returns fluctuate from one year to the next, a transfer from the buffer account ensures that your pension benefits are more stable.

Every month, an amount is transferred from your buffer account to your pension account. A number of mathematical formulas determine how the amount is calculated – that is what return you get on your pension account. This takes place in two stages:

The buffer account is used for the return that Danica achieves on your savings. Every month, we transfer a portion of the buffer account to the pension account. The remaining amount in the buffer account will act as a buffer at times when investment market returns fluctuate. That way, the return is equalised, as years with negative returns can often be offset against previous years with positive returns.

As your total return can be

either positive or negative, the balance of the buffer account and the total amount transferred from the buffer

account to the pension account can be positive or negative.

If you have a Tidspension scheme with guarantee, you ensure that the annual interest accrued on your pension account

will never be negative.

.

Content is loading

Content is loading